The GHG Protocol Scope 3 Revision: What the March 2026 update means

The GHG Protocol Scope 3 Standard was published in 2011. Since then:

- The European Green Deal was legislated,

- CSRD went from proposal to law to simplification

- SBTi became widely adopted worldwide.

How the world approaches corporate sustainability has shifted, but the methodology companies use to measure their value chain emissions had remained largely unchanged, until recently.

On March 31, 2026, the Phase 1 Progress Update of the Scope 3 Standard Revisions was published. It is the first substantive output from 42 working sessions held by the 65-member Technical Working Group across more than 20 countries. The final revision is not expected until late 2027, with adoption likely 2028 or later.

In this blogpost we are going to talk about the four most important revisions (of the 30 in total). These are still in draft so these are still subject to change.

- Disclosure of your Scope 3 data quality

- 5% exclusion cap

- Primary Data Share

- Labelling verified categories

- Category 15 increased coverage

- New category 16 for facilitated Emissions

What has changed?

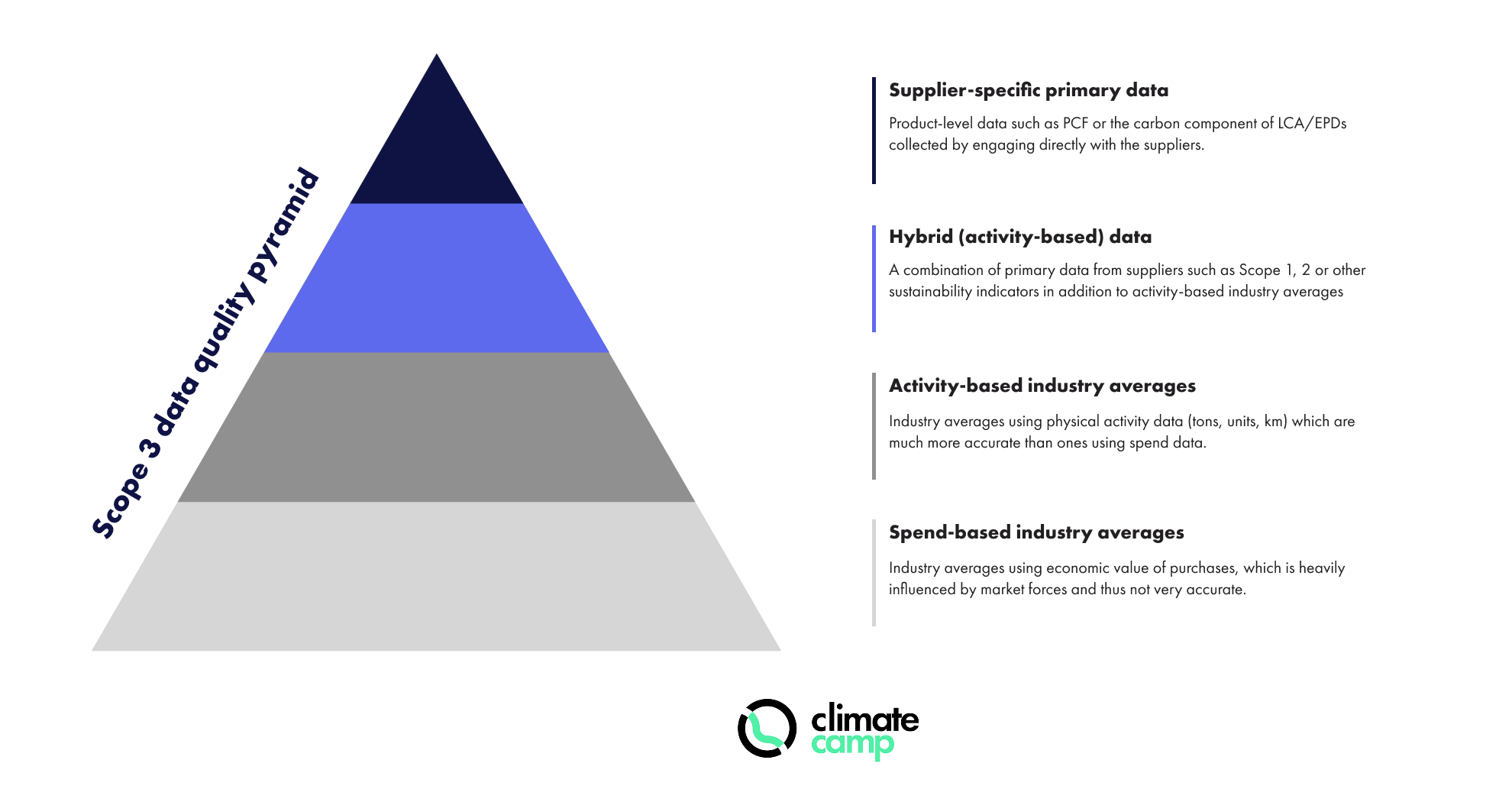

1. Your Scope 3 data quality will have to be disclosed.

Companies will need to break each Scope 3 category down by the following proposed data type: primary, hybrid, activity-based, or spend-based.

Today, your Scope 3 total sits in your sustainability report as a single number per category. After the updated revision, the data quality behind those figures becomes disclosed and comparable. Companies using supplier-specific data will have to say so on their reports. Investors, procurement counterparts, and evaluators will see the difference.

Hybrid data exists as a concept, but is not embedded in the Scope 3 standards yet.

Spend-based data tends to be the most readily available data for companies who want to comply with regulations and show their baseline publicly. Even though using spend-based data can help you draft a baseline quickly, if you or your customers want to set reduction targets, you might end up having an inventory that’s much larger than you initially estimated. Because of this, you will have to reduce even more, whilst current reduction timelines are already challenging.

Spend-based calculations do let companies map their hotspots, which is one of the reasons it's the dominant method for CSRD, CO2 Performance Ladder etc. The harder problem is what happens after the hotspots are known. To reduce on a spend-based number you have two options:

- Spend less, which is rarely a good choice if you want to grow,

- Switch to a lower-carbon product that often costs more, which then shows up as higher emissions in the inventory even when the physical carbon has dropped.

Spend-based and activity-based end up telling two different stories about the same reduction.

There is a related technical point in the revision: emission factors used in Scope 3 calculations cannot rely on cutoffs or exclusions greater than 5%, and regional factors must account for cross-border flows. In practice, that means a factor applied to a Polish supplier needs to reflect Poland's coal-heavy grid, not a blended "EU-27" average. Without the cross-border flows, your emission factor doesn’t reduce with the goods, because the carbon intensity can be drastically different between the production and buying location. Here’s a real-life example:

Mark is the CSO at a mid size German chemical company. His current Scope 3 platform pulls Cat 1 emission factors from Exiobase, 2014 base year, at the EU-27 level for "Manufacture of chemicals”. His single largest spend is a specialty material sourced from one supplier in Guangzhou. The factor Mark is using assumes EU electricity and EU process intensity. His actual supplier runs on a Chinese coal provincial grid.

Under the revised standard, that factor likely fails on three counts:

- the base year is too old,

- the industry bucket is too aggregated,

- the regional assignment does not follow the cross-border flow.

When running this in 2026, best practice is starting with labelling by category, document which method is in use where, and flag the categories where the spend-based data is predominant.

A quieter change in the same series: how supplier data gets split.

When a supplier hands you one company-wide emissions figure and you carve out "your share" of it, that's corporate-level allocation. The draft proposes restricting it. As written, you'd only be allowed to allocate a supplier's corporate-level data when that supplier is homogeneous, one with fairly uniform emissions across everything it does. For a diversified supplier, a single blended corporate number can't be cleanly attributed to the one product you actually buy, so corporate-level allocation would no longer be permitted for them.

Take a supplier that runs both a high-intensity aluminium smelter and a light-footprint logistics arm under one parent. Their corporate average sits somewhere in the middle, too low for the smelter output you buy, too high for anything else. Splitting that blended figure onto your purchase gives you a number that's wrong in both directions. Under the revision you'd need facility- or product-level data from them instead.

Overhead-type emissions that genuinely can't be tied to a product line (R&D, corporate functions...) can still be allocated. The restriction targets attributable emissions from diversified suppliers.

2. Only 5% of your Scope 3 emissions can be left out.

There are actually two coverage changes coming through at once:

- Before companies in practice reported their largest categories and justified the rest, but it’s being replaced with a materiality-based approach. If a category is material (a known emission hotspot) to your sector, it needs to be included no matter how small.

- The current standard asks you to "disclose and justify" exclusions. The revision replaces that with a hard rule: 95% of required Scope 3 emissions must be reported, and no more than 5% can be excluded cumulatively.

Most companies have excluded at least some Scope 3 categories because the data was hard to collect, the emissions seemed immaterial, or no one pushed back.

PCF data collection is a tiresome process for many companies, it requires significant time and financial investment. Even when an organization is willing, and in some cases required, to collect this from their suppliers, it might take a long process to educate suppliers, give them time to generate the required data and ultimately deliver it, to get there some years later.

According to the CDP, when a supplier is presented with data collection survey from multiple customers, the likely response range is around 71%. This however, does not cover whether or not the surveys requested the PCF data and if supplier has provided it.

This process does not need to be difficult to map, here are the steps:

- Initial mapping with your hotspots with spend-based data,

- For your material hotspots, move towards activity-based data. Improving your data quality by retrieving the quantity, volume and distance information is a good first step,

- Start primary data collection from your suppliers which are tied to your biggest hotspots

Even a rough estimate of what is currently excluded is enough to know whether you are over the 5% line. Once your strategy is set, data collection phase will make your data more reliable and actionable.

This is the part of Scope 3 work that goes from spreadsheet exercise to operational program and it's what ClimateCamp's platform was built to handle. We combine automated supplier pre-fill (pulling CCF, PCF and target data from public sources) with a dedicated supplier onboarding team that handles the calls and supplier education most procurement organizations can't resource internally.

One thing worth being precise about: the 5% applies only to required emissions.

The draft splits your Scope 3 into two buckets that have to be reported separately: required emissions (the prescriptive boundary, where the 95%/5% rule bites) and optional emissions (everything else, with no coverage floor). You can't dilute your coverage ratio by loading in easy optional categories, and you can't hide a missing required category behind a pile of optional ones. The denominator for your 5% is strictly the required set.

This matters most for the big, lumpy optional categories: indirect use-phase emissions in Category 11, and most of the new Category 16, which can dwarf everything else and would otherwise distort the picture. Keeping them in a separate column is what makes year-on-year and company-to-company comparison actually work.

3. Your improvement trajectory will be public.

The revision proposes a new metric called Primary Data Share (name tbd), which is the share of your Scope 3 inventory based on supplier-specific data rather than spend-based or industry averages. Companies will be expected to set and disclose annual improvement targets against it. Let’s take a look at an example.

Anna is Head of Sustainability at a mid-size beverage company:

The company buys 10,000 tonnes of aluminum per year for €25M.

- Spend-based data : €25M x Exiobase EU-27 metal factor = 50,000 tCO2e

- Activity-based data : 10,000 x industry average emission factor = 110,000 tCO2e

Neither of these numbers move their Primary Data Share. Only when they collect primary data from their suppliers they see the change:

- Supplier A (Norway) : supplies 4,000 tonnes at 2.5 tCO2e per tonne

- Supplier B (UAE) : supplies 4,000 tonnes at 11 tCO2e per tonne

- Supplier C (China) : supplies 2,000 tonnes at 18 tCO2e per tonne

Total with primary data drops to 90,000 tCO2e. Not only the company’s Primary Data Share improved, but now Anna can see where reduction opportunities sit. Supplier C, represents 20% of their volume but 40% of their aluminum emissions. This exercise, not only will this help Anna lower emissions by redistributing volumes but also better monitor the progress year-over-year.

Data quality will stop being an internal process choice and becomes an externally tracked performance metric. If your primary data share is low in 2028 or later, and shows no year-on-year improvement, your auditors, investors, and customers will read it.

The relationship with suppliers also changes, because building primary-data coverage usually means questionnaires, data systems, and in some cases contractual terms. It is also a likely assumption that some of your suppliers will not have PCF data readily available.

This is the prime example of why this process should be started in 2026 rather than in 2028 or later when its mandated. Reduction progress can take years and your suppliers are the key.

- Year 1: You reach out to your suppliers, they don’t have PCF data available.

- Year 2: They perform initial data gathering and report with spend-based data

- Year 3: Their data is of higher quality and they can work on collecting primary data for their calculations as well.

The practical first step is honestly small: document a baseline number for your current primary data share, even if it is 0, and write the year-on-year improvement into your roadmap.

4. Verified categories will have to be labelled as such.

As proposed, if you get any part of your Scope 3 inventory third-party verified, you'll have to say which part — using a simple label: Fully verified, Partially verified, or Not verified. The flip side is built in: if you verify nothing, you don't have to declare that. The label only kicks in once assurance enters the picture.

The practical read here is about scope, not effort. CSRD already pulls some Scope 3 into limited assurance for many companies. Rather than treating this as a new task, the useful question is which categories make sense to fold into the assurance scope you're already paying for — typically your largest, most defensible, activity-based categories — so the "partially verified" label points at the numbers you most want to stand behind.

5.Category 15 may now apply to you, even if you are not a bank.

In the new draft, Category 15 (investments / financed emissions) is proposed to apply to any company, not only financial institutions. A new Category 16 covers value chain activities that are not captured in Categories 3.1 to 3.15.

For holding companies, private-equity-backed businesses, and large corporates with diversified structures, this changes what is in scope. Joint ventures, equity stakes in other businesses, material investment portfolios. They all start to count.

*Company X, a German industrial machinery manufacturer:

- Has reported Scope 1, 2, and Categories 3.01 to 3.14 in its CSRD disclosure for years

- Has never touched Category 15 because it isn't a bank.

Under the revised standard, three things they previously excluded need to be assessed:

- A 35% stake in a chemicals JV in Shanghai,

- A corporate venture portfolio with positions in two clean-tech startups,

- A defined benefit pension fund with €400M of listed equity holdings.*

The Shanghai plant has a verified footprint of around 800,000 tCO2e per year, and proportionally consolidated at 35%, that adds 280,000 tCO2e to Company X’s Category 15, roughly double the entire Scope 3 the company reports today.

There's also a change to the maths, not just the boundary. As proposed, the denominator for proportional investment calculations includes both equity and debt, not equity alone. This brings Category 15 into line with PCAF. In practice, an investee's emissions get shared across everyone financing it, equity and debt holders alike, with the slices summing to the whole. The effect is that your attributed share reflects the company's full capital structure rather than just the equity portion, so the number you book can shift meaningfully depending on how leveraged the investee is. If your team already runs PCAF-style financed-emissions calculations, this is familiar ground; if Category 15 is new to you, it's worth knowing the attribution factor isn't simply your equity percentage.

6. Category 16: a new home for "facilitated" emissions

Alongside the Category 15 change, the draft proposes an entirely new category: Category 16 or "other value chain activities". These are emissions you influence but that don't fit anywhere in Categories 1 to 15. The defining case is facilitated emissions: emissions from a third-party activity where you earn direct, transactional income but never buy, sell, or own the thing itself.

Think brokerage and intermediary models, many financial services, and licensing. A licensor, for example, could use Category 16 to report the scope 1, 2, and 3 emissions of the activities its licensing enables. Insurance and underwriting are proposed to move out of Category 15 and into Category 16 too.

The important nuance: as drafted, almost all of Category 16 is optional, with one exception: oil and gas distributors, for whom it's required. So for most companies this is a "map it, understand it, decide whether to disclose it" exercise rather than a hard new obligation. But if your business model earns fees from activities you don't own. This is the category that finally has a place for them.

Summary

If your Scope 3 emissions are verified by a third party, you will need to disclose which categories were verified and by whom. CSRD already drags some Scope 3 assurance into your audit, so the more useful framing is which categories make sense to fold into the assurance scope you already have.

2026 may not be the year to publish a perfect Scope 3 number for everyone. It is the year to:

- Audit your inventory by data type. Know which categories sit on spend-based, activity-based, or primary data.

- Check what your emission factors actually reflect. Factors need to resolve at country level due to the new cross-country flow rule, supplier-specific where possible.

- Start supplier engagement now. Identify your top 30 to 50 suppliers and kick off a real data program. Waiting until the next revision means starting from zero with a long road to reduction.

- Map your Category 15 exposure with finance. Joint ventures, equity stakes, and investment portfolios now count toward Scope 3.

- Separate credits from your gross Scope 3 number. Retired credits get disclosed alongside the inventory, not netted into it. If you've been netting, the headline number will jump.

If you need help further refening your carbon footprint, taking into account the proposed revisions regarding data quality, Primary data share, or the fuller scope of coverage. ClimateCamp has helped over 100 companies map their initial footprints, improve data quality and forecasted Scope 3 decarbonization pathways.