SBTi’s Corporate Net-Zero Standard V2: What's changed?

On June 11, 2026, the SBTi published Version 2.0 of its Corporate Net-Zero Standard, the most significant rewrite since the framework began. By SBTi's own account, 42% of the sections in V2 are entirely new, and the rest are modified. For most companies with a validated target, this means a rebuild of how their decarbonization strategy has to be put together.

It also lands at a moment when the gap between climate ambition and delivery is hard to ignore. In March 2024, SBTi changed the status of 239 companies, including Microsoft, P&G, Unilever, and Walmart, to "commitment removed" after they missed the deadline to submit validated targets. In a survey behind that round, roughly half of responding companies pointed to Scope 3 as the thing making net-zero targets too hard to set.

V2 is in large part, SBTi's answer to that problem: keep the ambition, but make the value-chain work more structured and more deliverable. This blogpost condenses the more than a 100 page document, into its most key takeaways. If you want to read the full document, follow this link.

The timeline, so you can plan around it

V2 will come into effect as of 1 February 2028. There is however a transition window. From Q1 2027 you can submit targets for validation against either V1.3.1 or V2, and V1.3.1 submissions remain open until the end of 2027. After that, V2 is mandatory for all submissions.

In practice, that gives you two routes. If you need a validated target soon, you can still use V1.3.1 and keep some of its flexibilities (like a combined Scope 1 and 2 target) while adopting V2 innovations early.

If your target is up for renewal, the SBTi notes that companies with existing 2030 targets should start building for V2 target-setting cycles (2030–2035) starting in 2028 to ensure adequate supplier and structural lead times.

Net Zero V2 isn't the only thing changing

The Net-Zero Standard sits inside a complex inter-linked regulatory frame, which is part of why getting your data house in order has compounding value:

- The GHG Protocol Scope 3 revision is being written in parallel.

- CSRD limited assurance survived the Omnibus simplification.

- CBAM has set a commercial precedent for installation-level supplier data.

- The EU's Empowering Consumers Directive restricts generic "climate-neutral" product claims based on offsetting, with member-state application from September 2026.

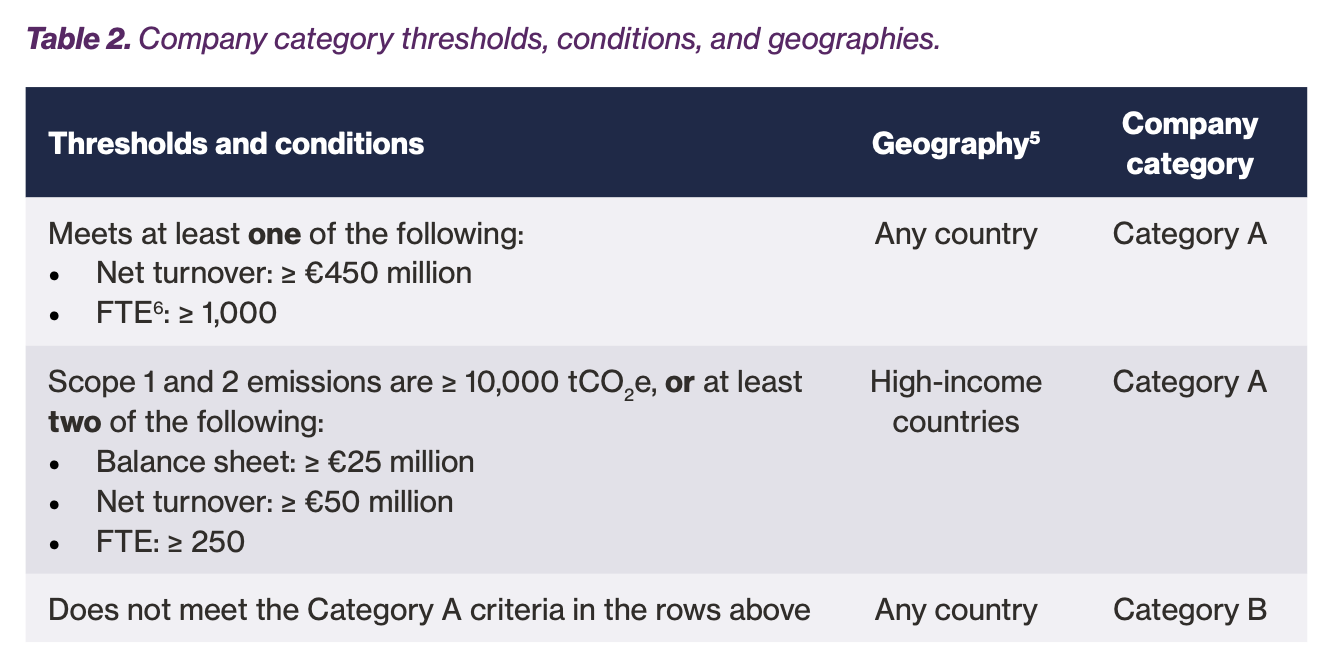

1. First question under V2: which category are you?

V2 retires the separate SME route and replaces it with formal company categorization: Category A and Category B. Different categories have different obligations based on turnover, geography, emissions, and employee thresholds.

This matters immensely because several of the heaviest lifts are restricted strictly to Category A companies (broadly, larger companies or medium enterprises in high-income economies). Crucially, near-term Scope 3 targets are required only for Category A companies, leaving Category B enterprises exempt from mandatory Scope 3 near-term target setting. Furthermore, mandatory third-party limited assurance over data , formal public disclosure of transition plans , and the post-2035 carbon-removal duty all sit squarely within Category A requirements. Category B operates on lighter minimum criteria.

So the first practical step is working out which category you fall into, because that determines which of the rules below actually bind you.

2. Why does SBTi V2 split Scope 1 and Scope 2 targets?

Under V1 you could set a single combined Scope 1 and 2 target. V2 forces you to separate them: a Scope 1 target covering 100% of direct emissions, and a Scope 2 target covering 100% of purchased electricity, heat, steam, and cooling. The combined number is gone, and with it the ability to greenwash progress on one scope with the other.

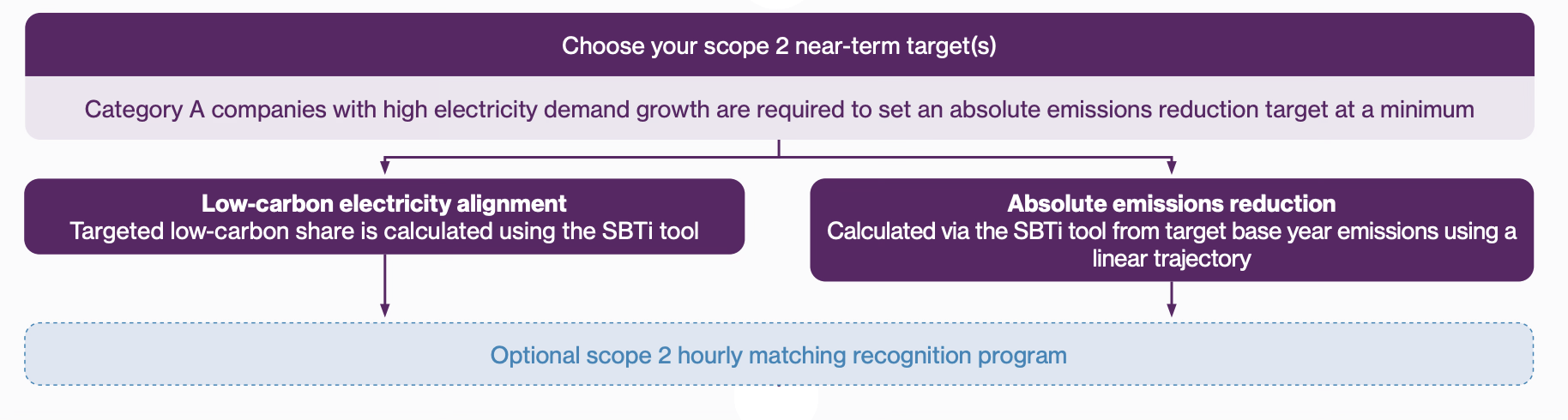

Scope 2 also becomes more strict

- Alignment targets move from "renewable" to "low-carbon" electricity,

- The emissions-intensity option is removed

- Scope 2 emissions targets are now based on the location-based (physical) inventory rather than the market-based one. Where market instruments can count toward delivery, they have to meet conditions such as geographic matching and a 15-year limit on the age of the generating asset. Companies growing electricity demand fast (above roughly 20% a year) are pushed toward emissions targets specifically.

Consider a Spanish pharmaceutical manufacturer with sites in Madrid, Barcelona, and Cork. Its combined Scope 1+2 target reads −42% by 2030 and looks on track. This is largely because around 80% of its electricity is covered by Nordic hydro guarantees of origin. Underneath that blended figure, Scope 1 has moved only −8%, because the gas boilers and HVAC in two of three sites haven't been touched.

Under V2, three things change at once.

- The two scopes split, so the slow Scope 1 trajectory becomes visible on its own for the first time.

- The Scope 2 emissions target is now assessed on the location-based inventory, so imported Nordic certificates no longer flatter the headline the way market-based accounting did.

- And for instruments to count toward delivery, they have to match the market where the electricity is consumed. Spanish and Irish load can't be greened with Nordic attributes.

This means for a lot of companies, Scope 2 changes from being an energy procurement exercise to a multi-year structural decision about where electricity is actually sourced from.

3. What replaces the 67% rule for Scope 3 in SBTi V2.0?

This is the change that touches the most companies. Under V1 you could build a Scope 3 target around roughly two-thirds of your value-chain emissions and justify leaving the rest out. V2 replaces that fixed-percentage threshold with a significance-based approach: you have to cover every Scope 3 category that represents at least 5% of your Categories 1–14 emissions. A category being awkward to collect data for is no longer a reason to exclude it.

There are defined escape hatches, specific optional exclusions are allowed within named categories (3, 7, 8, 9, 10, and 14) where a company genuinely can't influence the outcome, but each one has to be reported and justified. Category A companies additionally have to identify and quantify their emissions-intensive activities and report any that make up 5% or more of Scope 3.

The honest first move here is small but decisive: get a category-level read of your inventory. Which categories sit on spend-based, activity-based, or primary data, and how much of the total each represents. That tells you which categories cross the 5% line and where you're exposed.

PCF data collection from suppliers is slow and resource-heavy, and supplier survey response rates are far from universal or qualitative. This is the part of Scope 3 work that turns sustainability into a manual spreadsheet exercise,rather than an operational decarbonization program. This is what ClimateCamp makes more efficient: automated supplier pre-fill from public CCF, PCF, and target data, paired with a supplier-onboarding team that educates suppliers and validates private carbon data such as PCFs or sustainabiliy indicators.

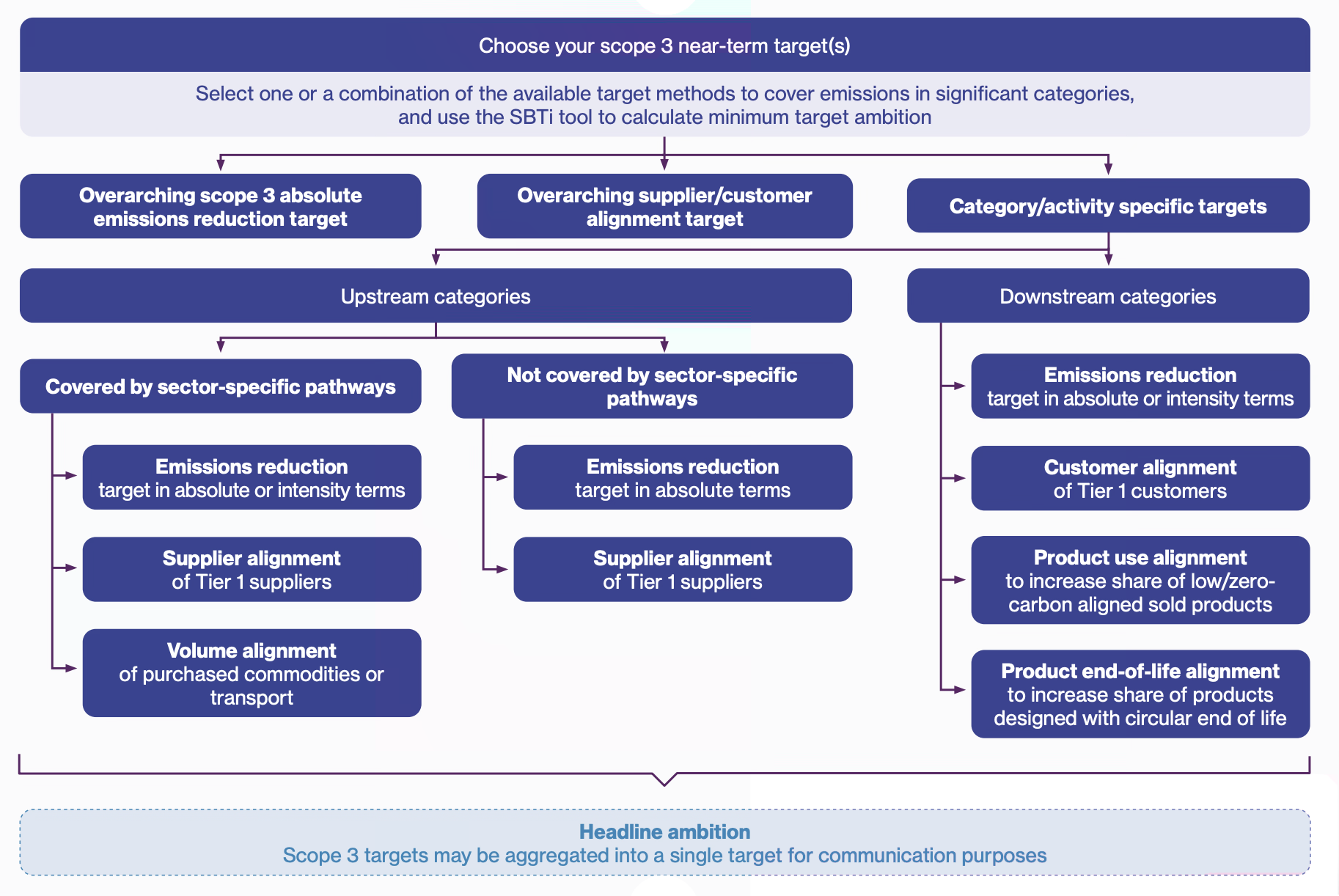

4. New ways to set Scope 3 targets

V2 doesn't just change the boundary; it broadens how you're allowed to set Scope 3 targets.

The old supplier-engagement target grows into wider supplier and customer alignment pathways. This measures the share of your suppliers or customers that are "in transition" or "net-zero aligned", alongside new methods tied to commercial levers: volume, product use, and product end-of-life. The spend-based and physical-intensity Scope 3 methods (the old 7%-a-year intensity route) were removed, because there aren't science-based reference pathways behind them.

There's also a tightly constrained exception for Category 11 (use of sold products) where no downstream option is reasonably applicable, but it needs SBTi approval, mandatory long-term targets, transition-plan milestones, and annual emissions reporting. Under V2's new structural breakdown, long-term Scope 3 targets (as well as long-term Scope 2 targets) are now explicitly optional for all companies, shifting the mandatory focus onto clear 5-year near-term delivery windows.

This means SBTi is formalizing what leading companies are already doing: pushing key suppliers to hold their own validated, 1.5°C-aligned targets. For suppliers, the question stops being whether a major customer will ask about emissions and becomes when, and whether they can answer credibly.

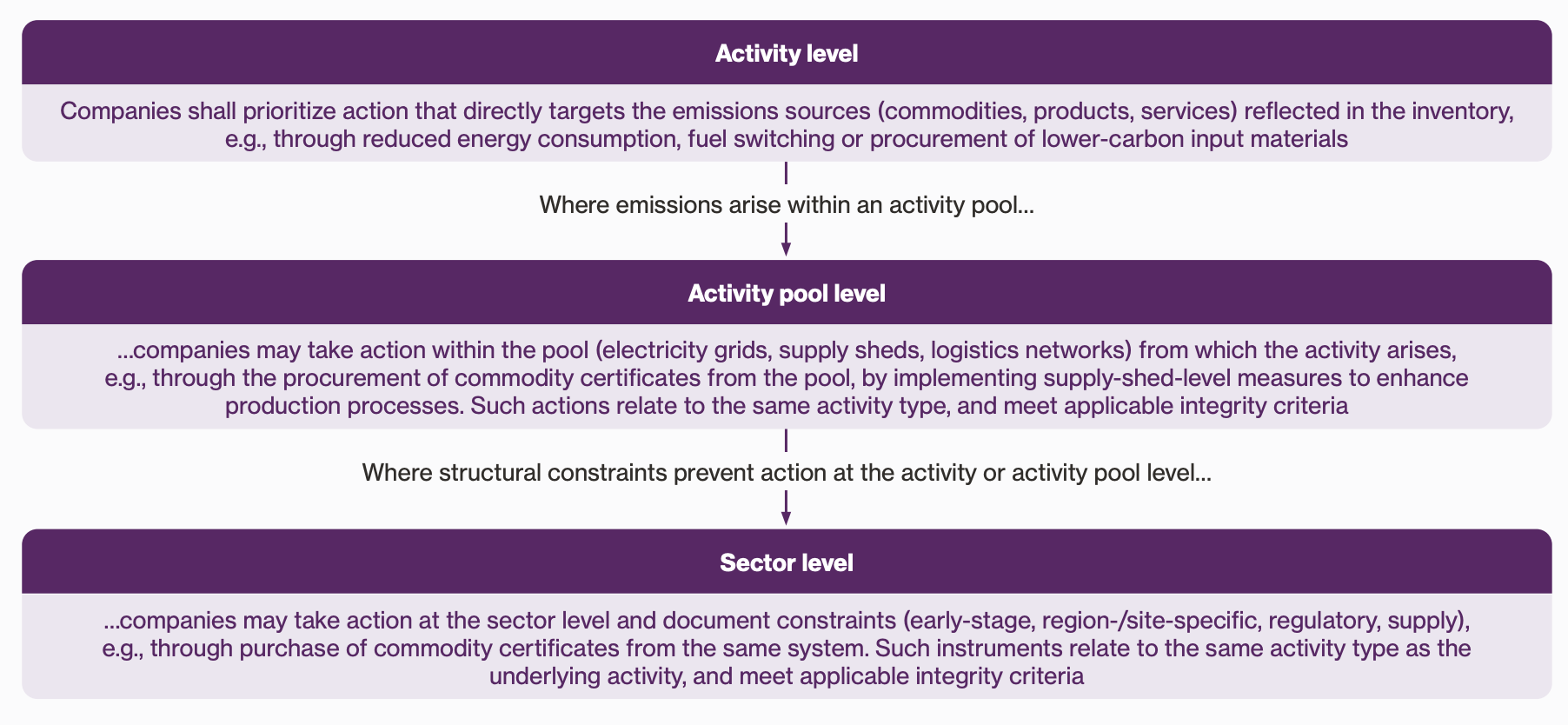

5. The implementation hierarchy: how you're allowed to deliver

One of the biggest genuinely new ideas in V2 is the implementation hierarchy, which is a ranked order for the actions that count toward your targets. Direct, activity-level emissions reductions in your own operations and value chain come first. Actions within shared systems ("activity pools") or at the sector level are only permitted where structural constraints make direct reduction impractical. Around this sits a set of integrity criteria for any action, project, or market instrument: it has to be additional, verifiable, free of double-counting, and reflected in your physical inventory.

The practical consequence is that V2 closes the door on treating a certificate purchase as interchangeable with a real reduction. Market instruments still have a role, including different chain-of-custody models such as mass balance and book-and-claim, but they're ranked below direct action and fenced with conditions, rather than being a free substitute.

6. Best-efforts delivery, governance, and assurance

V2 reframes what a target is. Targets are now pursued on a "best-efforts basis," with companies expected to use all available levers, surface the barriers they hit, and report on them transparently. That's paired with a continuous-improvement loop: structured annual progress reporting, plus an end-of-cycle assessment that evaluates where you landed against the target and what got in the way.

Underneath that, V2 makes mandatory what V1 mostly recommended. Net-zero governance, board-level accountability, and a transition plan become explicit requirements. For most companies this overlaps heavily with what CSRD and ESRS E1 already ask for, so the transition plan and the assurance scope can usually be built once and shared. Third-party limited assurance over inventories and target-setting metrics is mandatory for Category A companies. A validated number without an audited plan behind it won't pass.

7. Carbon credits and "ongoing emissions responsibility"

This is the area the early commentary most often gets wrong, so it's worth being precise.

Carbon credits still cannot be used to hit your reduction targets. V2 treats high-integrity credits and climate contributions as a complement to cutting your own emissions, never a substitute. What used to be called Beyond Value Chain Mitigation (BVCM) has been absorbed into a broader framework SBTi now calls Ongoing Emissions Responsibility (OER). More importantly, it's a voluntary recognition framework, not a new obligation to fund external mitigation.

The one hard, forward-looking duty is narrower than the "credits become mandatory" headlines suggest: from 2035 onward, Category A companies face a mandatory carbon-removal requirement for residual emissions on the path to net-zero (removals specifically, not avoidance credits), with detailed rules on storage durability and double-counting. If you've historically used offsets to bring a reported number down, V2 removes that room: the credit story sits alongside the inventory, and gross emissions are reported gross.

What to do next, target or no target

The "perfect" V2 Scope 3 report isn't publishable this year for most companies. The data isn't there, suppliers aren't ready, and the supporting guidance is still landing. But waiting until V2 is mandatory is the expensive mistake, because the supplier and removal work both take years. The steps that pay off now:

- Confirm your company category. It determines which V2 requirements actually apply to you, so settle this before anything else.

- Take an honest, category-level inventory. Know which Scope 3 numbers are spend-based, activity-based, or primary, and how much of the total each drives. That's the baseline V2 will measure improvement against, and it tells you which categories cross the 5% line.

- Start real supplier engagement. Identify the suppliers behind your biggest Category 1–14 hotspots and kick off a data program now. Response rates to cold questionnaires are low; a system and a dedicated onboarding approach change that.

- Plan Scope 2 as a sourcing decision, not a procurement one. Map where your electricity is actually consumed and whether your instruments will survive the location-based, same-market, generator-age tests.

- Build the plan and assurance once. Treat the transition plan, third-party assurance, and your CSRD/ESRS work as one workstream rather than three parallel ones, to avoid double cost in money and time.

If you need help preparing your GHG inventory to assess to possibility for reduction across all scopes, as well as help setting targets and building the decarbonization, we at ClimateCamp would love to help you. Get in touch and let's discover how we can help you hit your goals.